Mat Tax Rate In India

Pin On Income Tax

Income Tax Diary In 2020 Income Tax Tax Paying Taxes

Sujit Talukder Incometaxdiary Twitter In 2020 Income Income Tax Deduction

What Is Minimum Alternate Tax Mat News Budget 2020 News Mat Calculation

Prefilled Itr For Taxpayers Convenience Tax Refund Tax Deducted At Source Income Tax Return

No Penalty For Late Filing Of Income Tax Return Income Tax Tax Return Income

Tax 30 on rs.

Mat tax rate in india.

10 Changes In Itr 1 Filing In 2019 Income Tax Dividend Income Tax Refund

Pin On Income Tax

India Shrinks Corporate Income Tax Rates Fm

Changes In Itr 2 And Itr 3 For Showing Scrip Wise Separate Ltcg Income Tax Income Income Tax Return

How To Calculate Net Income 12 Steps With Pictures Net Income Formula In 2020 Net Income Income Net

Important Aspects Of Tds On Cash Withdrawal Under Section 194n After Union Budget 2019 Budgeting Banking Institution Income Tax

It Works Global Income Disclosure Statement It Works It Works Global It Works Distributor It Works

Reason To Buy Gold Online Share Trading Stock Market Stock Broker

Pin On Graphic Representation Of Market Brands And Many More

Income Tax Diary Income Tax Income Income Tax Return

Income Tax Diary Budgeting Income Tax Life Insurance Policy

Income Tax Diary In 2020 Income Tax Income Awareness Campaign

Section 115baa And 115bab New Tax Rate For Companies

37th Gst Council Meet Key Highlights Accoxi Tax Consulting Council Highlights

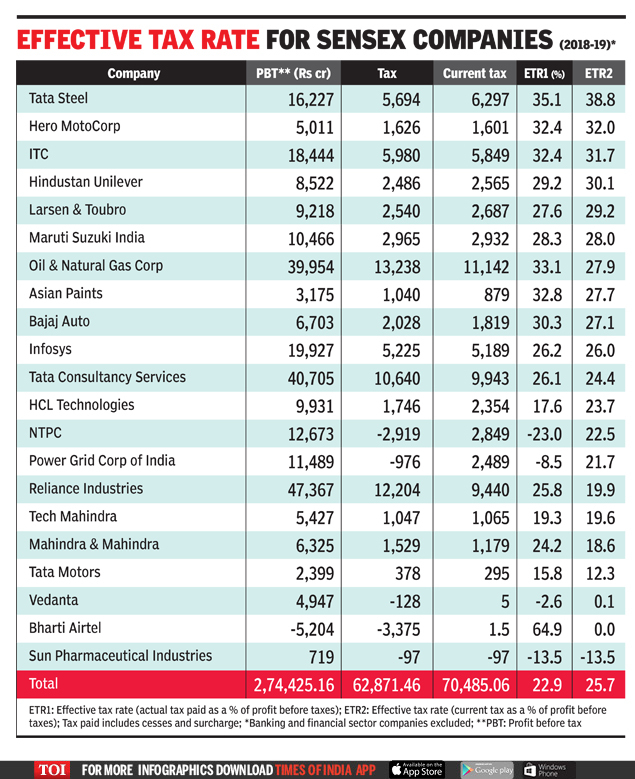

Many Top Firms Actually Pay Less Than 25 Tax Times Of India

Income Tax Diary In 2020 Income Tax Income Tax Return Income

Pin On Research Panel Investment Advisers

Hra Tax Exemption Not Allowed For Rent Paid To Mother Itat Tax Exemption Tax Household Expenses

Goods And Services Tax Goods And Service Tax Goods And Services Indirect Tax

Source : pinterest.com