Mat Tax Rate For Ay 14 15

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

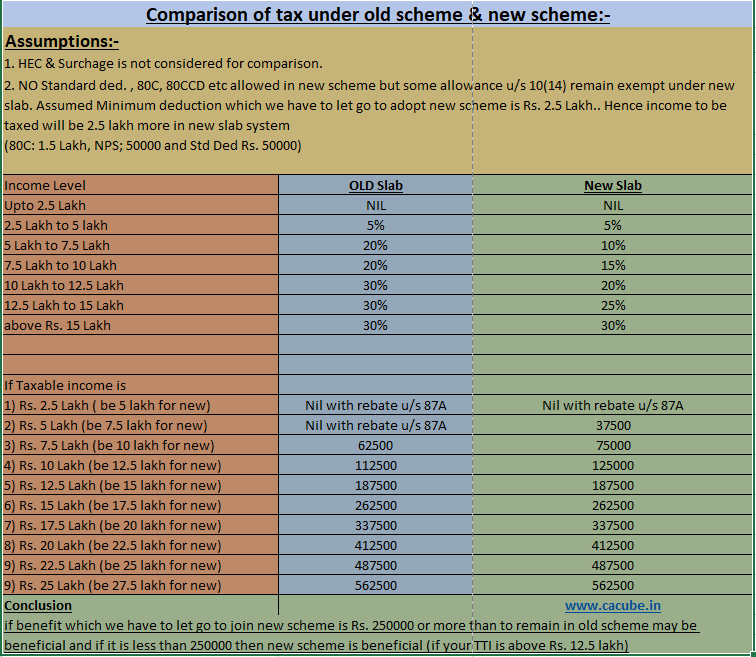

Income Tax Slab Rates Marginal Relief Mat For A Y 2015 2016 Taxing Tax

What Is Minimum Alternate Tax Mat Tax Mat Calculation

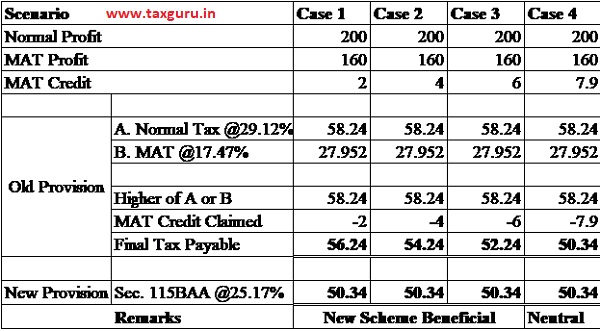

New Corporate Taxation Regime Section 115baa And Mat

Rates Of Income Tax For Fy 2020 21 Assessment Year 2021 22 Cacube

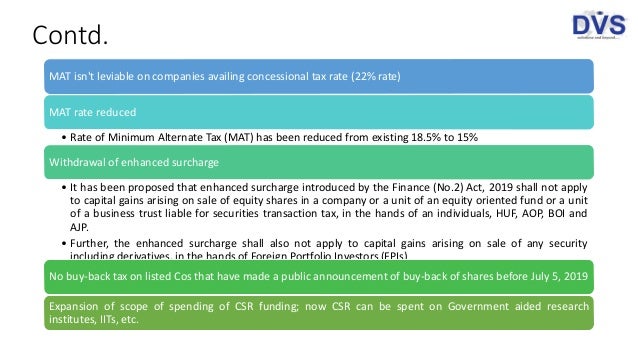

Sitharaman has now brought down the.

Mat tax rate for ay 14 15.

What Is Minimum Alternate Tax Mat Calculation Mat Tax Credit

New Corporate Taxation Regime Section 115baa Mat

Minimum Alternate Tax Mat Objective Applicability Calculation Of Mat Credit Finacbooks

Strategic Analysis Of Amended Corporate Tax Rate Regime

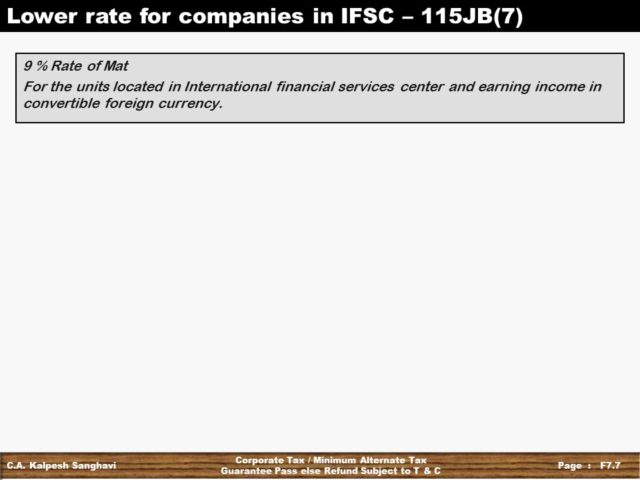

Minimum Alternate Tax Mat Section 115jb

Https Papers Ssrn Com Sol3 Delivery Cfm Ssrn Id1759907 Code1612178 Pdf Abstractid 1759907 Mirid 1

Section 115baa And 115bab New Tax Rate For Companies

Fin 315 Exam 5 Answers Unc Greensboro Common Stock Unc Greensboro Exam

Pin Pa Recipe

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Https Icaiahmedabad Com Pdf September 17 E Newsletter Abad Wicasa Pdf

Minimum Alternate Tax

All You Need To Know About Mat Applicability To Companies Faceless Compliance

Income Tax Amendments New Provisions Of Finance Act 2020

Minimum Alternate Tax Mat Civilsdaily

Tolerance Range In Transfer Pricing

Ca Final Question Bank Dt Minimum Alternate Tax Mat

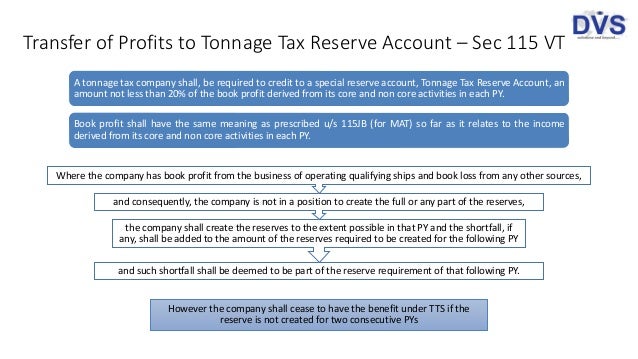

Tonnage Taxation Scheme

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcsoj4ih9dmulxl7ekfnhgqd0iy4kcd410zi1gj4rw9jc0m69pfd Usqp Cau

Source : pinterest.com