Mat Rate For Ay 2019 20

Income Tax Diary In 2020 Income Tax Tax Paying Taxes

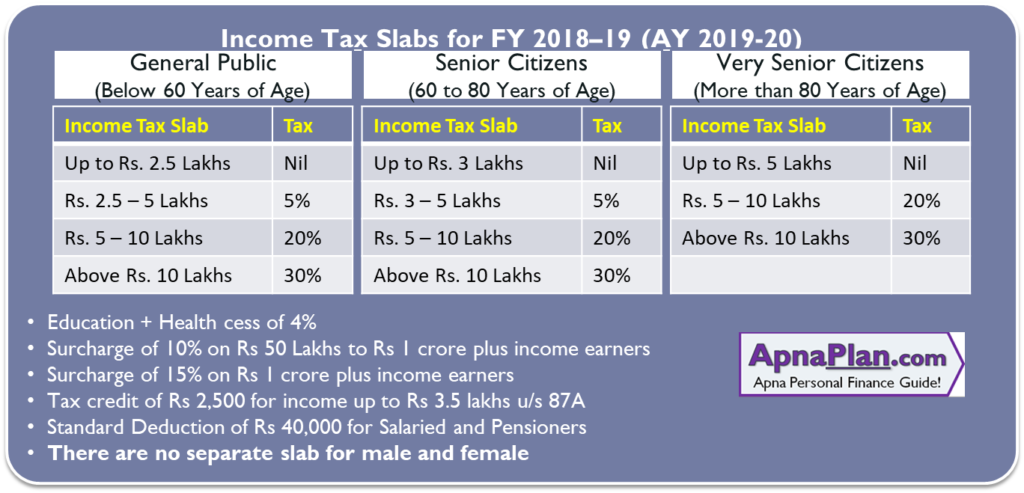

Income Tax Calculator For Fy 2018 19 Ay 2019 20 Excel Download Apnaplan Com Personal Finance Investment Ideas

Prefilled Itr For Taxpayers Convenience Tax Refund Tax Deducted At Source Income Tax Return

Income Tax Deductions For Salaried Employees Fy 2019 20 In 2020 Income Tax Tax Deductions Tax Deductions List

Tds Rate Chart Fy 2018 19 Ay 2019 20 Tds Deposit Return Due Dates Interest Penalty Simple Tax India

Income Tax Rate For Partnership Firm Fy 2019 20 Ay 2020 21 Income Tax Rate For Partnership Firm Fy 2019 20 Ay 2020 21

For fy 2019 20 tax payable is computed at 15 previously 18 5 on book profit plus applicable cess and surcharge.

Mat rate for ay 2019 20.

No Penalty For Late Filing Of Income Tax Return Income Tax Tax Return Income

Latest Income Tax Slab Rates Fy 2019 20 Ay 2020 21 Basunivesh

Changes In Itr 2 And Itr 3 For Showing Scrip Wise Separate Ltcg Income Tax Income Income Tax Return

Current Income Tax Rates For Fy 2019 20 Ay 2020 21 Sag Infotech

10 Changes In Itr 1 Filing In 2019 Income Tax Dividend Income Tax Refund

Sujit Talukder Incometaxdiary Twitter In 2020 Income Income Tax Deduction

Latest Tds Rates For Fy 2018 19 Ay 2019 20 Bravery Truth Rate Bravery Truth

What Is The Income Tax Slab Rate For Ay 2020 21 Quora

Income Tax Rate For Ay 2020 21 Fy 2019 20 Updated

1 Tds Rate Chart Fy 2019 20 Ay 2019 20 Notes To Tds Rate Chart Fy 2019 20 Ay 202 Investment Quotes Investing Infographic Money Book

Income Tax Rate For Llp Ay 2020 21 Fy 2019 20 Read Llp Due Dates

Income Tax Deductions List Fy 2019 20 List Of Important Income Tax Exemptions For Ay 2020 21 Tax Deductions Tax Deductions List Income Tax

Summary Of Slab Deductions Under Income Tax Ay 2020 21

Latest Tds Rate Chart Fy 2019 20 Ay 2020 21 Basunivesh Tax Deducted At Source Accounting And Finance Chart

Public Provident Fund Scheme 2019 In 2020 Public Provident Fund Fund Schemes

Income Tax Diary Budgeting Income Tax Life Insurance Policy

Income Tax Diary Income Tax Income Income Tax Return

Hra Exemption Is Allowed On Actual Payment Of Rent Income Tax Actual Payment

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gct289duxbbxtkloxcjog4dwvp3zfumhq7y4xqqpamtgboggnshq Usqp Cau

Source : pinterest.com