Mat Rate For Ay 2018 19

Changes In Itr 2 And Itr 3 For Showing Scrip Wise Separate Ltcg Income Tax Income Income Tax Return

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Set Off Of Bf Loss Mat Credit Adjustments Under New Tax Regime

New Corporate Taxation Regime Section 115baa And Mat

Interest Sec 234a 234b 234c For Fy 2018 19 Of Income Tax Act Excel Download

One Of The Most Renowned Tax Consultants On Whom An Individual Can Rely Upon Call Us On 91 9810065014 Company Law Mat Tax Consulting Online Taxes Tax Advisor

19 on annual earnings above the paye tax.

Mat rate for ay 2018 19.

Summary Of Slab Deductions Under Income Tax Ay 2019 20

89 1 Relief Calculator For Financial Year 2018 19 Simple Tax India

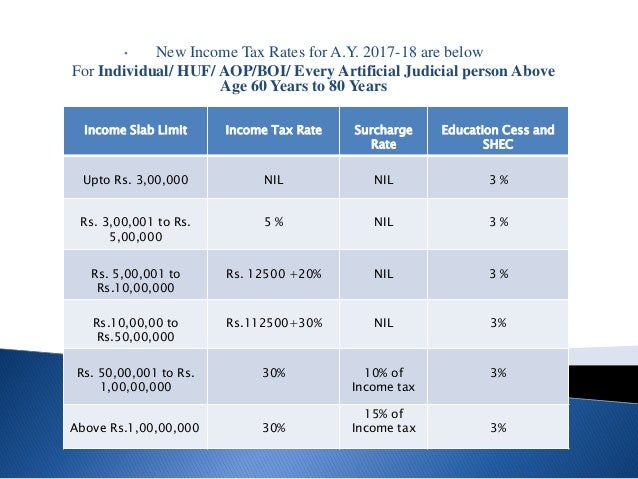

Income Tax For Fy 2017 18 Or Ay 2018 19

Income Tax Calculator For Fy 2018 19 Ay 2019 20 Excel Download Apnaplan Com Personal Finance Investment Ideas

Income Tax Diary In 2020 Income Tax Income Awareness Campaign

Income Tax Rate For Companies Ay 2019 20 Fy 2018 19 Indiafilings

Tds Rate Chart Fy 2018 19 Ay 2019 20 Tds Deposit Return Due Dates Interest Penalty Simple Tax India

Budget 2017 18

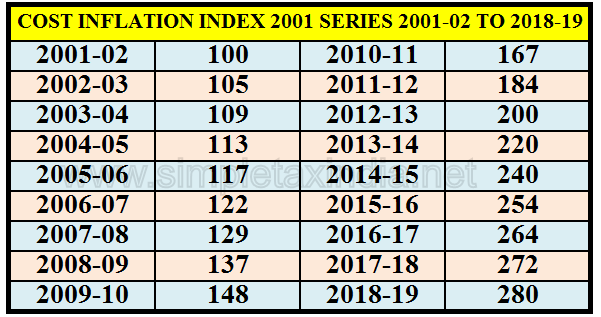

Cost Inflation Index Fy 2018 19 Released Simple Tax India

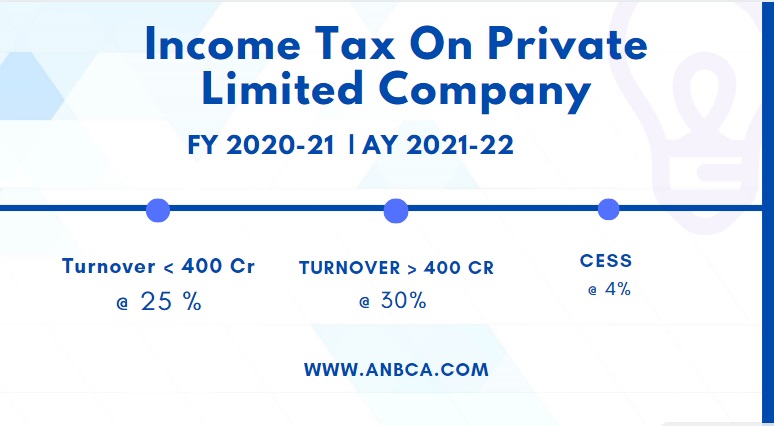

Income Tax Rate On Private Limited Company Fy 2020 21 Ay 2020 21

Http Commerce Du Ac In Web Uploads E 20 20resources 202020 201st M Com 20sem 20iv Mr Chetan Minimum 20alternate 20tax Pdf

Nativo Content Home Remedies Yoga Stretches Health Tips

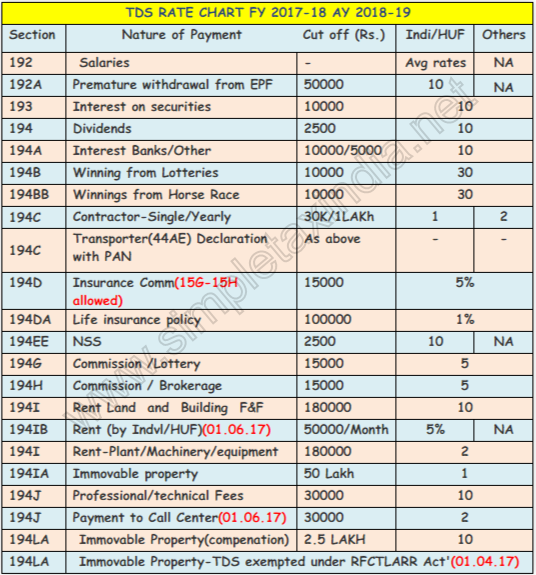

Tds Rates Chart Fy 2017 18 Ay 2018 19 Tds Deposit Return Due Dates Interest Penalty Simple Tax India

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Tds On Salaries For Fy 2017 18 Ay 18 19 U S 192 Income Tax Act 1961 Simple Tax India

Extension Of Income Tax Return Due Date For Ay 2019 20

Extend Due Dates For Tax Audit And Income Tax Return Filing

Income Tax Rates For Financial Year 2019 20 And 2020 21

1

Source : pinterest.com