Mat Rate For Ay 2013 14

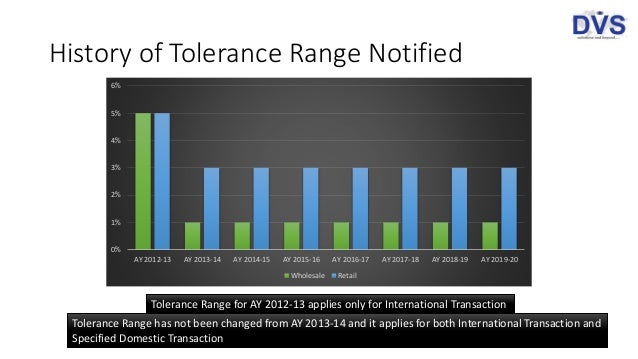

Tolerance Range In Transfer Pricing

Minimum Alternate Tax

Pdf Financial Fair Play Implications For Football Club Financial Reporting

Hard Up Families Seek Ppi Payouts The Independent The Independent

Https Dera Ioe Ac Uk 21483 1 Academies August 2014 Accounts Return Guide Pdf

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Tax liability as per the mat provisions are given in sec 115jb 18 5 of book profits plus 4 education cess plus a surcharge if applicable.

Mat rate for ay 2013 14.

Https Www Ijcb Org Journal Ijcb20q4a2 Pdf

Eur Lex 52020pc0408 En Eur Lex

Income Tax Rates Ay 2014 15 Fy 2013 14 Smart Paisa

Https Www Mtw Nhs Uk Wp Content Uploads 2018 10 Agenda And Reports Part 1 September 2018 Complete Pdf

Increasing Rate Of Mat Reducing The Mat Credit

Https Www Pat Nhs Uk About Us Trust Board Meetings 2014 Jun Boardpack Trust Board Partb 1 June 2014 4 Pdf

Monthly Visibility Report July August 2014 Unesco Digital Library

Income Tax Slab Of Last 20 Years From Ay 2001 2002 To Ay 2021 2022 Financial Control

Pdf Located Accountabilities In Technology Production

Https Www Nic Org Uk Wp Content Uploads Cfe With Cover And Contents Pdf

High Resolution Laser Doppler Imager Moorldi2 Hir Moor Instruments

Https Www Napier Ac Uk Media Worktribe Output 1261586 High Shear Rate Rheometry Of Micro Nanofibrillated Cellulose Pdf

Http Researchonline Lshtm Ac Uk 4645398 1 Early 20academic 20achievement 20in 20children 20with 20isolated 20clefts Pdf

Https Www Oxfordshire Gov Uk Cms Sites Default Files Folders Documents Childreneducationandfamilies Educationandlearning Schools Ourworkwithschools Pupilplaceplan Pupilplaceplandata Pdf

Https Publications Jrc Ec Europa Eu Repository Bitstream Jrc121476 Jrc121476 Jrc Commonshareholding Final Pdf

Https Www Ema Europa Eu En Documents Variation Report Angiotensin Ii Receptor Antagonists Sartans Article 31 Referral Chmp Assessment Report En Pdf

Minimum Alternate Tax Mat Section 115jb

Https Www Kch Nhs Uk Doc Corp 20 20346 1 20 20bod 20agenda 20and 20papers 20jul 2029 202014 Pdf

Pdf Effectiveness Of Mat Pilates Or Equipment Based Pilates Exercises In Patients With Chronic Nonspecific Low Back Pain A Randomized Controlled Trial

Source : pinterest.com