Mat Rate For Ay 2012 13

Income Tax Rates Ay 2012 13 Fy 2011 12 Smart Paisa

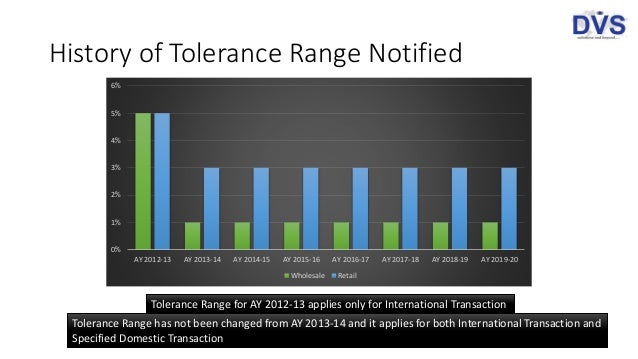

Tolerance Range In Transfer Pricing

Surcharge And Cess Is To Be Calculated After Deducting Mat Credit U S 115jaa From Tax On Assessed Income

Assessment Of Hindu Undivided Family Ppt Download

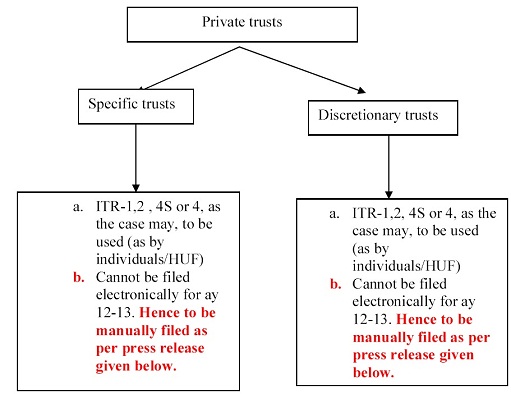

Taxation Of Private Trust Tax Planning

Income Tax Slab Of Last 20 Years From Ay 2001 2002 To Ay 2021 2022 Financial Control

In each finance bill the government increased the rate of mat and now this rate has increased to 18 5 in ay 2013 14 from 7 5 in ay 2001 02 and simultaneously kept reducing the difference between the mat and normal rate to reduce the eligibility of mat to the companies.

Mat rate for ay 2012 13.

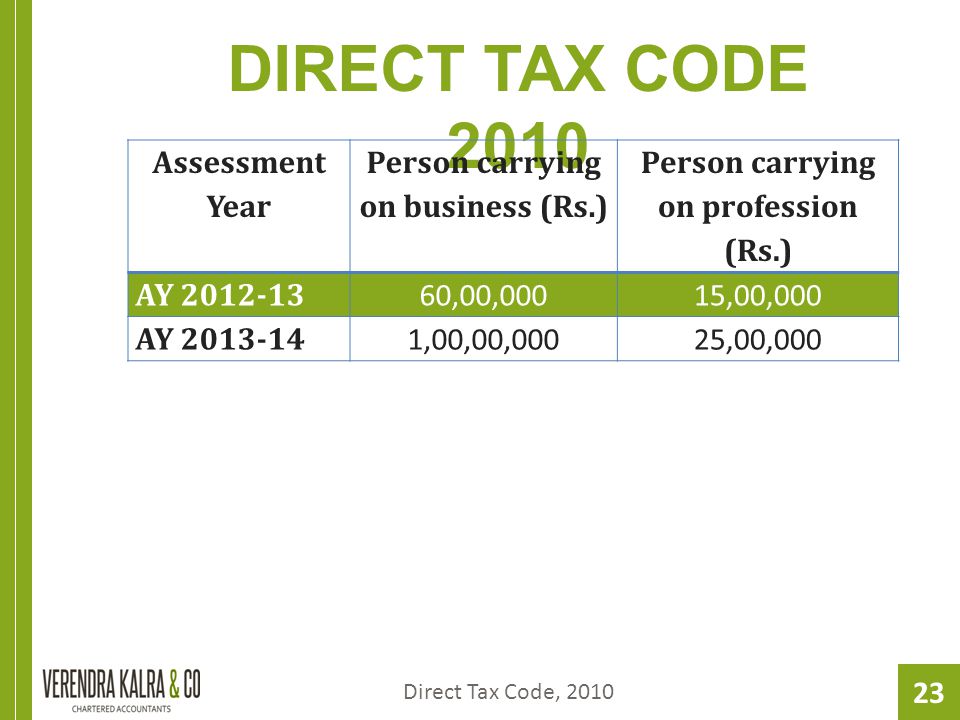

Presentation On Direct Tax Code 2010 Presented By Ca Verendra Kalra Organised By University Of Petroleum And Energy Studies Dehradun On Dec 14 Ppt Download

1969 Ford Mustang 428 Cobra Jet Convertible Car Pictures Mustang Ford Mustang Convertible Ford Mustang Shelby Cobra

Fabric Storage Oilcloth Laminatedcotton Mjhq Fabric Storage Fabric Shop Display Organize Fabric

Hqfq498jtzzgwm

Tour De France 2012 Preview Road Cc

The Lanchester Equations Of Warfare Explained Larry L Southard Ppt Video Online Download

Pdf The Body And Pedagogy Beyond Absent Moving Bodies In Pedagogic Practice

Kate Beckinsale Photos Photos The 54th Annual Grammy Awards Arrivals Grammy Fashion Nice Dresses White Short Dress

Http Www Southend Nhs Uk Media 61311 Annual Report 2011 12 Final Pdf

Https Www Tandfonline Com Doi Pdf 10 1080 01446193 2020 1726978

E Filing Of Income Tax Returns Tax Audit Reports For A Y 2013 14

How To Apply Online For Re Sending Of Cpc Intimation U S 143 1 154

Pdf Landslip Remediation Of Fairlight Cove Brighton Cliff Msc Environmental Geology

What Is Wireless Charging And Do I Need It Smartphones The Guardian

Https Www Nice Org Uk Guidance Cg98 Evidence Addendum Pdf 2490921037

Https Www Royalberkshire Nhs Uk Downloads Gps Gp 20protocols 20and 20guidelines Maternity 20guidelines 20and 20policies Postnatal Postnatal 20info 20homebirth2 20pack Pdf

Implementation Of The Who Surgical Safety Checklist And Surgical Swab And Instrument Counts At A Regional Referral Hospital In Uganda A Quality Improvement Project Lilaonitkul 2015 Anaesthesia Wiley Online Library

Pdf The Use Of Gps Analysis To Quantify The Internal And External Match Demands Of Semi Elite Level Female Soccer Players During A Tournament

Http Eprints Whiterose Ac Uk 106567 3 Kennedy 20hill 20feeling 20numbers Pdf

Source : pinterest.com