Mat Rate For Ay 2009 10

What Is The Applicable Minimum Alternate Tax Mat Rate For Ay 2020 21

Https Assets Publishing Service Gov Uk Media 5e8dc82686650c18cc99f228 Yorkshire Water Pr19 Redetermination Statement Of Case 02 04 2020 Pdf

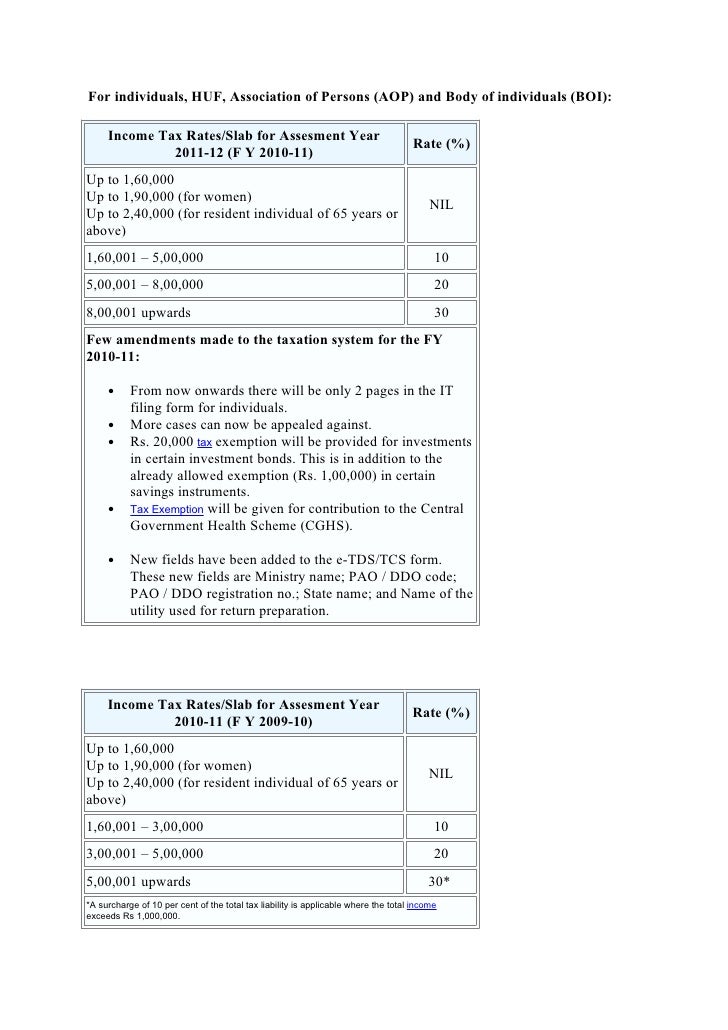

Income Tax Slabs Fy 2010 11

Pdf A 10 Year History Of Perinatal Care At The Brockington Mother And Baby Unit Stafford

Https Www2 Deloitte Com Content Dam Deloitte In Documents Tax In Tax Minimum Alternate Companies Noexp Pdf

Https Tc Copernicus Org Articles 14 4653 2020 Tc 14 4653 2020 Pdf

M01729 which you were given when your test centre registered you for the mat and which you wrote on the front of your mat test paper.

Mat rate for ay 2009 10.

Income Tax Slab Of Last 20 Years From Ay 2001 2002 To Ay 2021 2022 Financial Control

Https Www Nice Org Uk Guidance Cg76 Evidence Full Guideline 242062957

Https Www Pwc Com Gx En Asset Management Publications Pdfs Pwc Real Estate Going Global 2016 Pdf

Income Tax Rates Ay 2009 10 Fy 2008 09 Smart Paisa

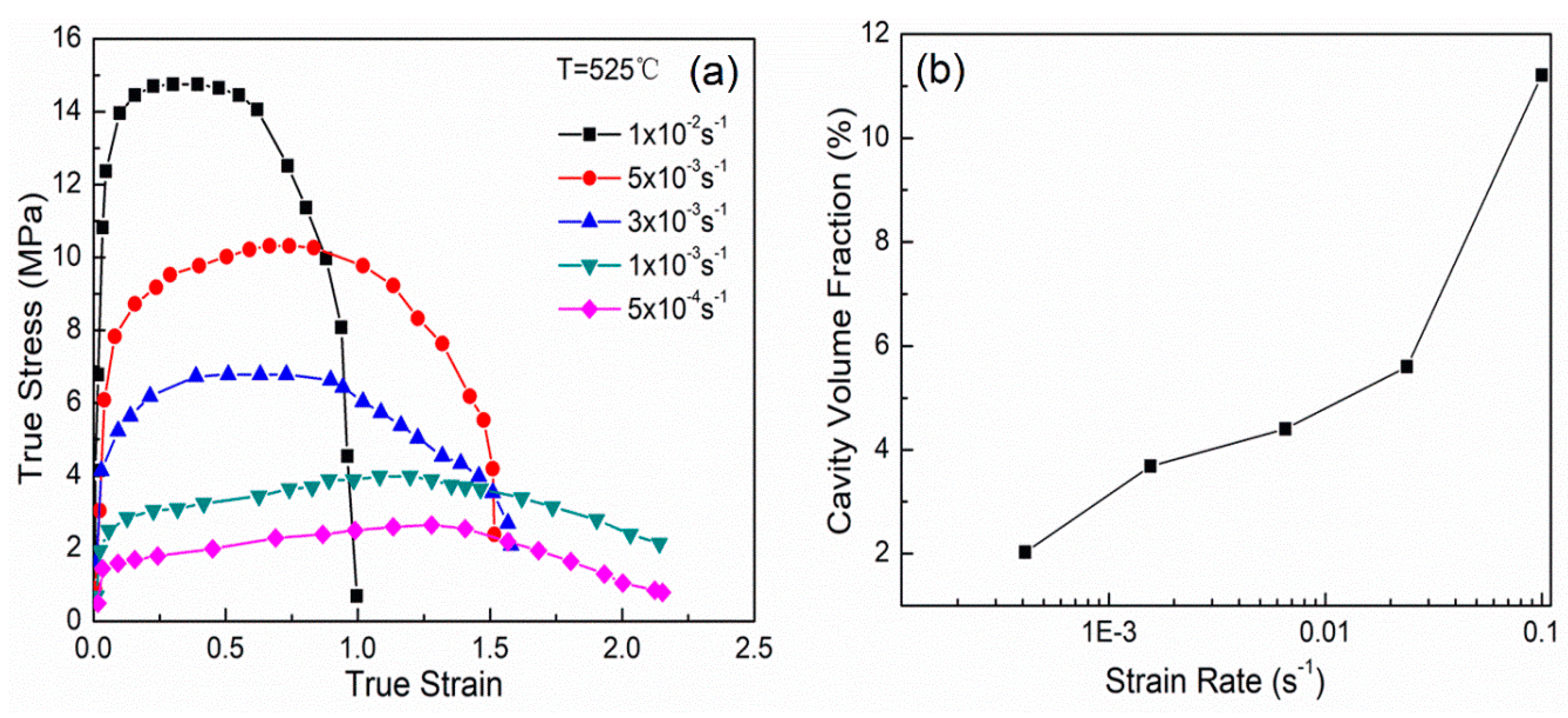

Metals Free Full Text Recent Development Of Superplasticity In Aluminum Alloys A Review Html

Pdf Heart Rate Variability Hrv Biofeedback A New Training Approach For Operator S Performance Enhancement

Pdf Short Term Versus Long Term Impact Of Managers Evidence From The Football Industry

Https Unfccc Int Sites Default Files Resource Bur 20report Final Pdf

Educational Marginalization In The Uk Unesco Digital Library

Monthly Visibility Report July August 2014 Unesco Digital Library

Http Www In Kpmg Com Taxflashnews Kpmg Flash News Elitecore Technologies Pvt Ltd 2 Pdf

Https Ec Europa Eu Docsroom Documents 17190 Attachments 1 Translations En Renditions Native

Honey As A Topical Treatment For Wounds Jull Ab 2015 Cochrane Library

Http Www Ocr Org Uk Images 15871 Copyright Acknowledgements Booklet June 2010 Pdf

Https Www Eos Oes Eu Downloads Eos Annual Report 2017 2018 Web Pdf

Pdf Understanding Luxury Consumption In China Consumer Perceptions Of Best Known Brands

Http Dissemination Echa Europa Eu Biocides Activesubstances 0009 08 0009 08 Assessment Report Pdf

Https Www Nic Org Uk Wp Content Uploads Cfe With Cover And Contents Pdf

Https Www Repository Cam Ac Uk Bitstream Handle 1810 278380 A 20review 20of 20recent 20work 20on 20discharge 20characteristics 20during 20plasma 20electrolytic 20oxidation 20of 20various 20metals Pdf Sequence 4

Source : pinterest.com