Mat Format Income Tax

Provision For Income Tax Definition Formula Calculation Examples

Guide To Minimum Alternate Tax For Ind As Compliant Companies

Income Tax Form Of 4 4 Is Income Tax Form Of 4 4 Any Good Five Ways You Can Be Certain In 2020 Income Tax Return Tax Forms Income Tax

Minimum Alternate Tax Mat Section 115jb

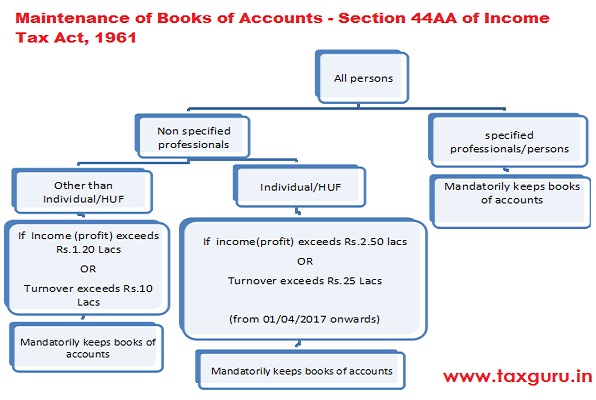

Maintenance Of Books Of Accounts Who Has Where Up To When

Reward Over Risk Trading Signals Trading Signals What To Sell Creating Passive Income

Total marginal relief 19 99 295 19 50 000 49 295.

Mat format income tax.

Income Tax Form Download In Excel Format Why You Must Experience Income Tax Form Download In In 2020 Tax Forms Income Tax Signs Youre In Love

Tax Return Fake Tax Return Income Tax Return Income Statement

Income Tax Calculation Formulas Excel Income Tax Computer Notes Income

Surcharge And Cess Is To Be Calculated After Deducting Mat Credit U S 115jaa From Tax On Assessed Income

One Of The Most Renowned Tax Consultants On Whom An Individual Can Rely Upon Call Us On 91 9810065014 Company Law Mat Tax Consulting Online Taxes Tax Advisor

Advance Tax Under Income Tax A Complete Guide

Dissecting Section 80m Of The Income Tax Act The Known And The Unknown Lexology

Calculation Of Mat Credit Applicability Of Minimum Alternate Tax

Income Tax Form Of Bd Eliminate Your Fears And Doubts About Income Tax Form Of Bd In 2020 Income Tax Return Income Tax Tax Forms

Income Tax Calculation Form Year 4 4 Seven Things To Know About Income Tax Calculation Form In 2020 Income Tax Things To Know Income

Income Tax Amendments New Provisions Of Finance Act 2020

American Expats Mark These Tax Deadlines On Your Calendar Medical Debt Tax Deadline Income Tax

Income Tax Ay 18 19 Mat Minimum Alternative Tax Lecture 1 Youtube

Rent Receipt For Income Tax Purposes Microsoft Word Template Receipt Template Invoice Template Receipt

Income Tax On Intraday Trading

Income Tax Calculator For Fy 2018 19 Ay 2019 20 Excel Download Apnaplan Com Personal Finance Investment Ideas

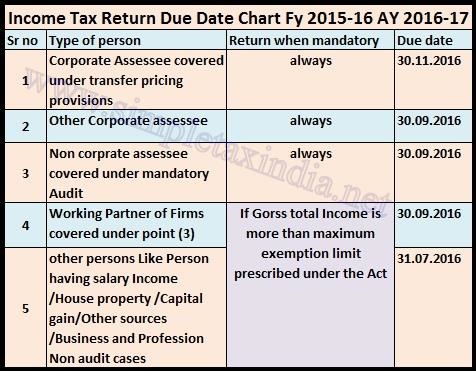

Due Date To File Income Tax Return Ay 2016 17 Fy 2015 16 Simple Tax India

Income Tax Form E Filing Malaysia 5 Things To Avoid In Income Tax Form E Filing Malaysia In 2020 Tax Forms Income Tax Income

Https Encrypted Tbn0 Gstatic Com Images Q Tbn And9gcsoj4ih9dmulxl7ekfnhgqd0iy4kcd410zi1gj4rw9jc0m69pfd Usqp Cau

Source : pinterest.com