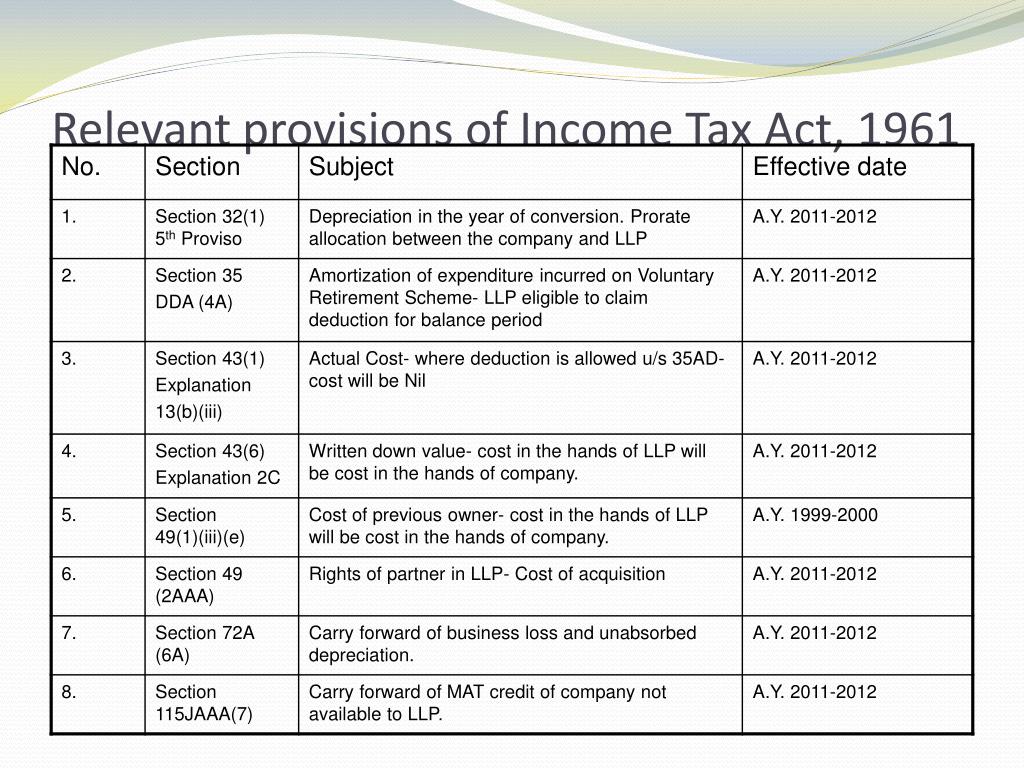

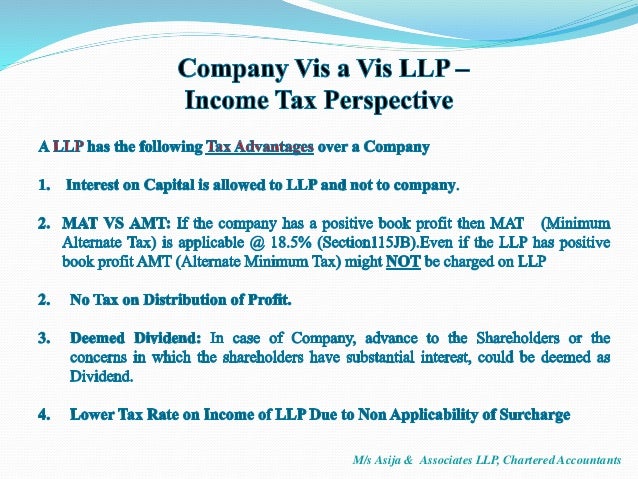

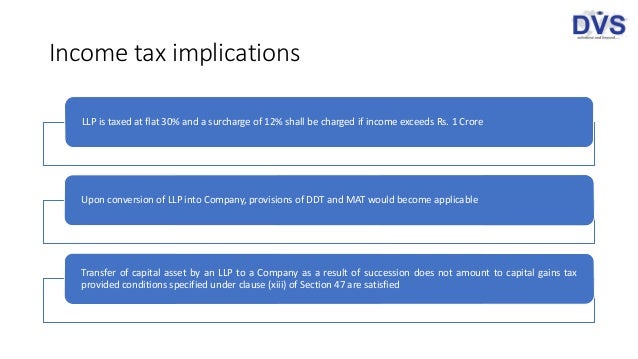

Mat Applicability On Llp

Formation Conversion Changes In Limited Liability Partnership Ppt Download

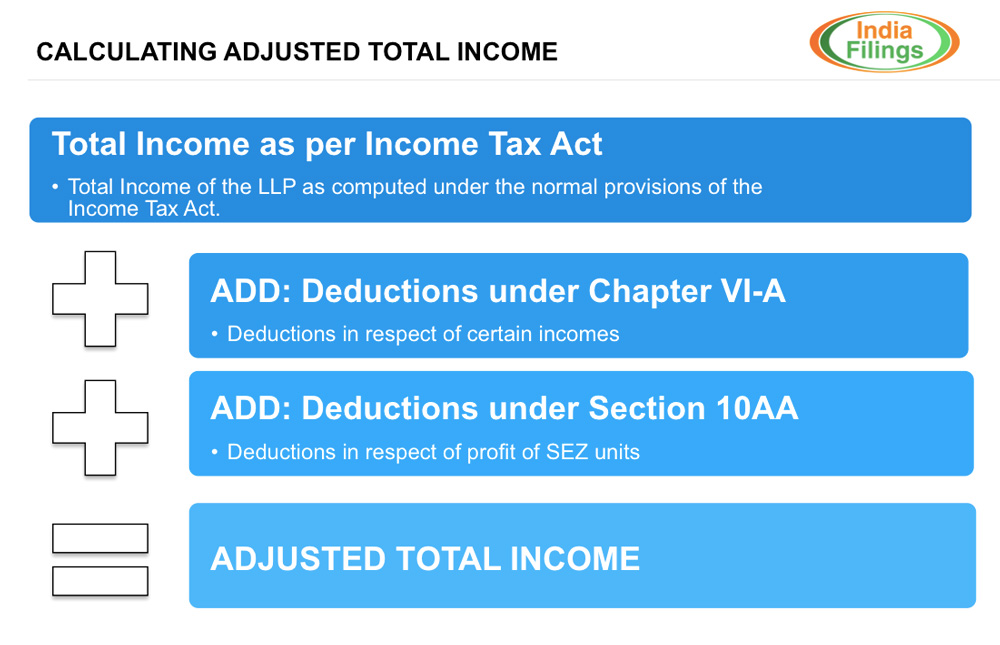

What Is Minimum Alternate Tax Mat Indiafilings

Taxation Of Llps Business Reorganisation Of Llp Ca Saurabh Shah Direct Tax Refresher Course Organized By Wirc Baroda 3 June Ppt Download

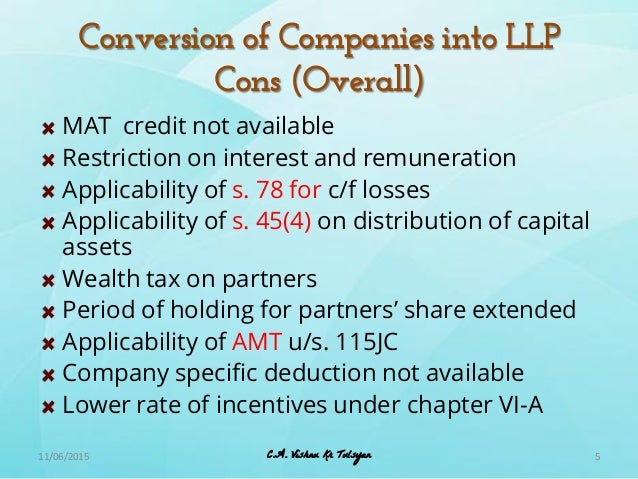

Pros And Cons Of Conversion Into Llp

All You Need To Know About Mat Applicability To Companies Faceless Compliance

Formation Conversion Changes In Limited Liability Partnership Ppt Download

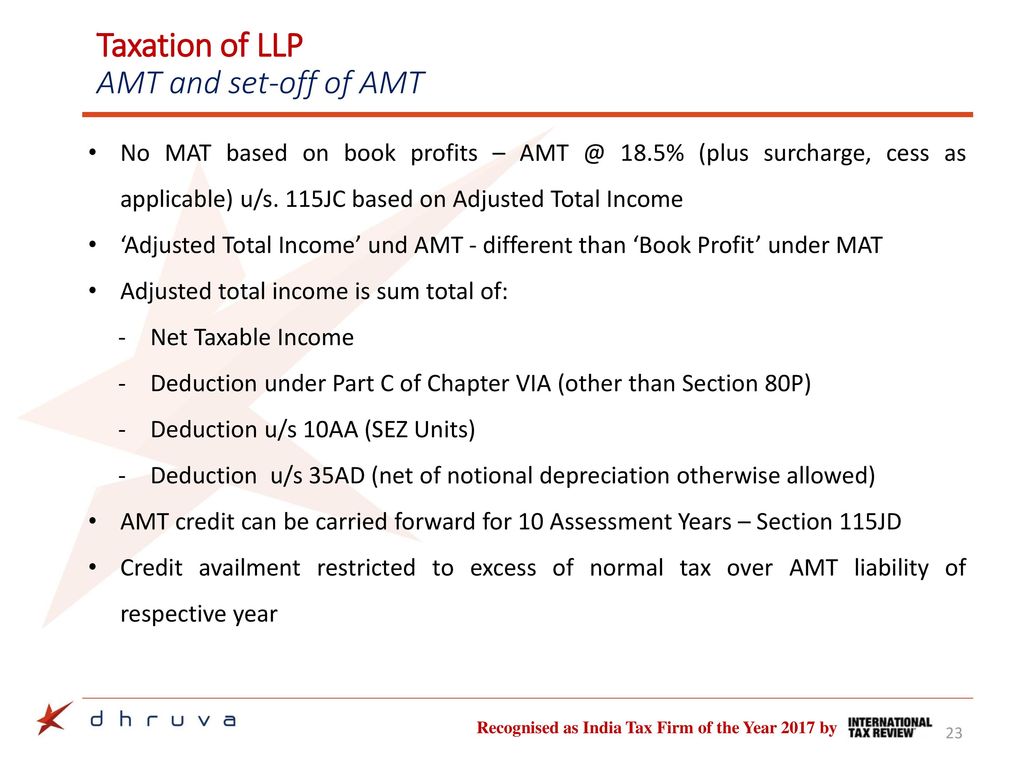

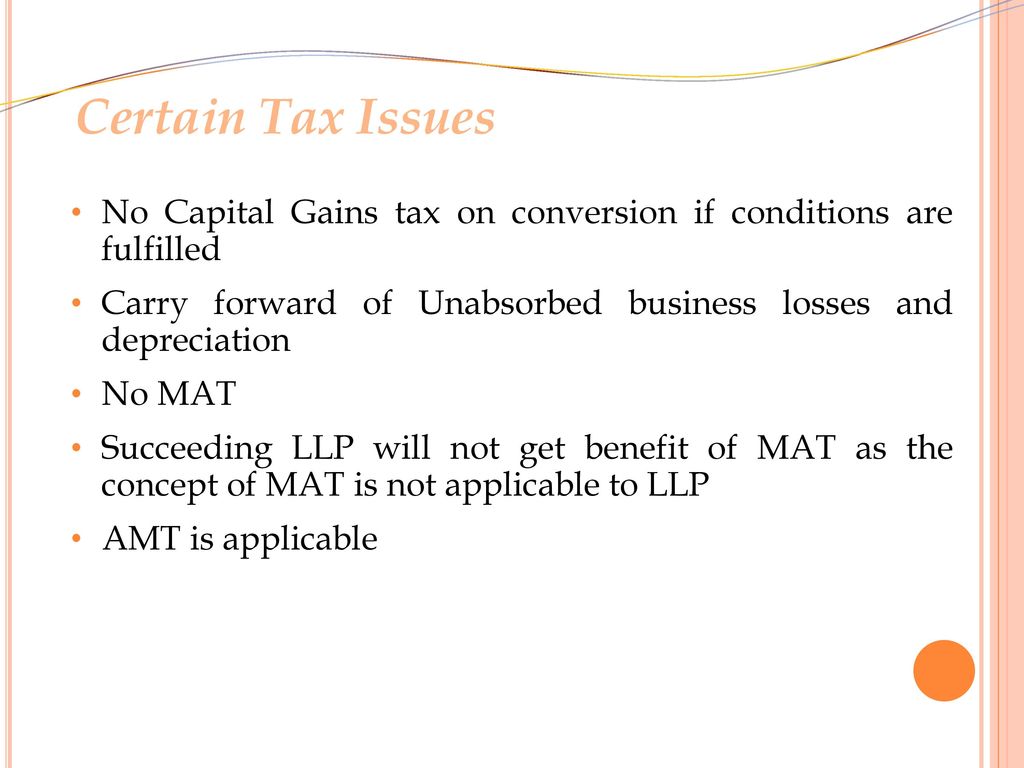

Similar to company llp paying amt can claim its credit for 10 assessment years.

Mat applicability on llp.

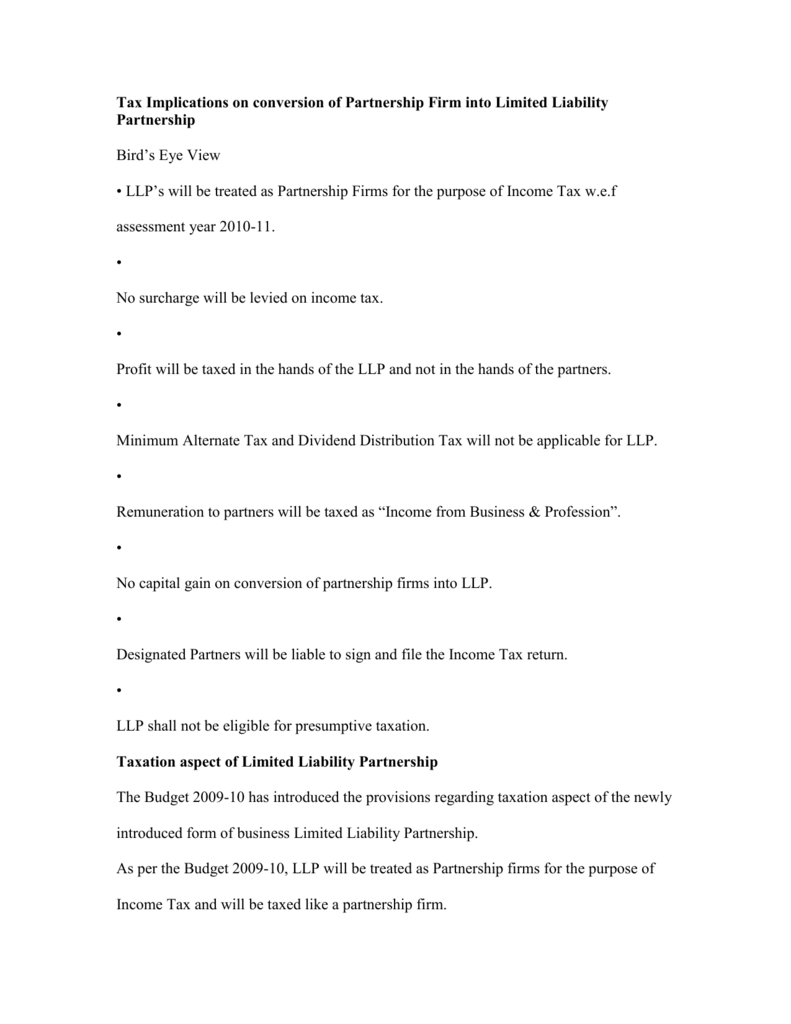

Implications For Conversion Of Partnership Firm Into Llp

Business Reorganizations And Restructuring Including Conversion Of Private Limited Company Or A Partnership Into A Llp And Tax Issues Direct Tax Convention Rajkot Ppt Video Online Download

Demystifying Llp Conversion Ppt Download

Mat As An Employer Hr And Employment Conference For School Leaders

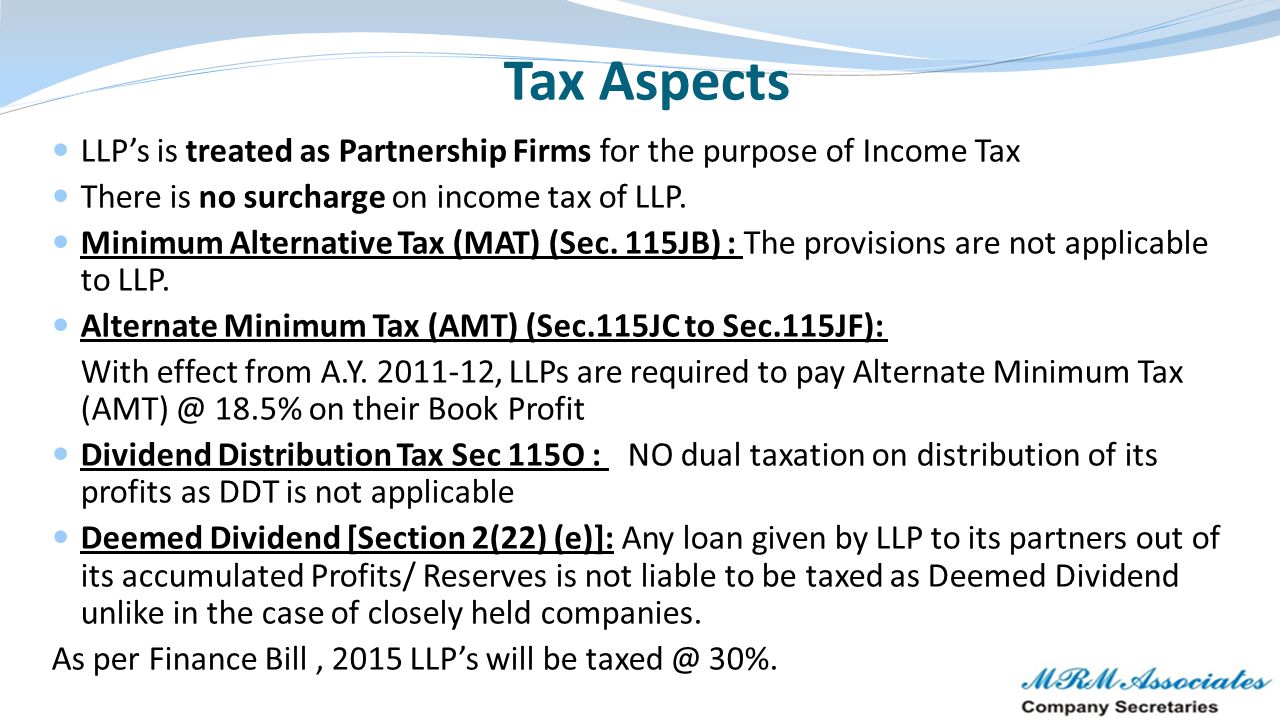

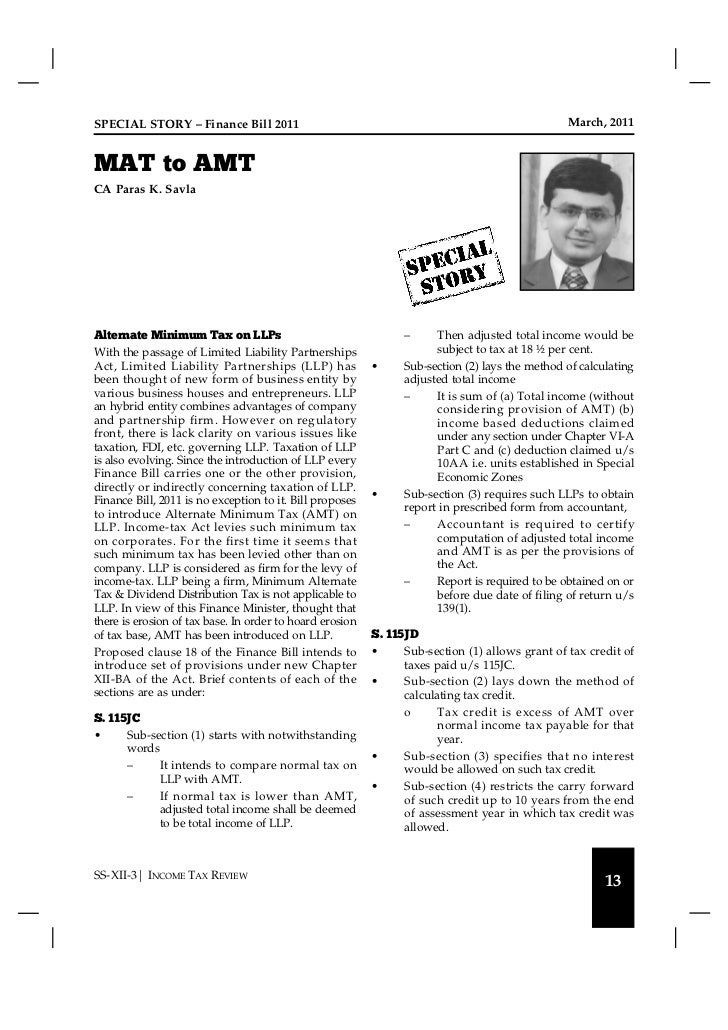

Mat To Amt On Llp

Taxation Of Limited Liability Partnerships Ca Vinod Jain B Com H Fca Fcs Fcwa Llb Disa Central Council Member Icai Mobile E Mail Ppt Download

A Private Company To A Limited Liability Partnership Llp Ppt Download

The Limited Liability Partnership Llp Is An Alternative Corporate Business Vehicle That Provides The Benefits Of Limited Liability But Allows Its Members Ppt Download

Ppt A Private Company To A Limited Liability Partnership Llp Powerpoint Presentation Id 2265298

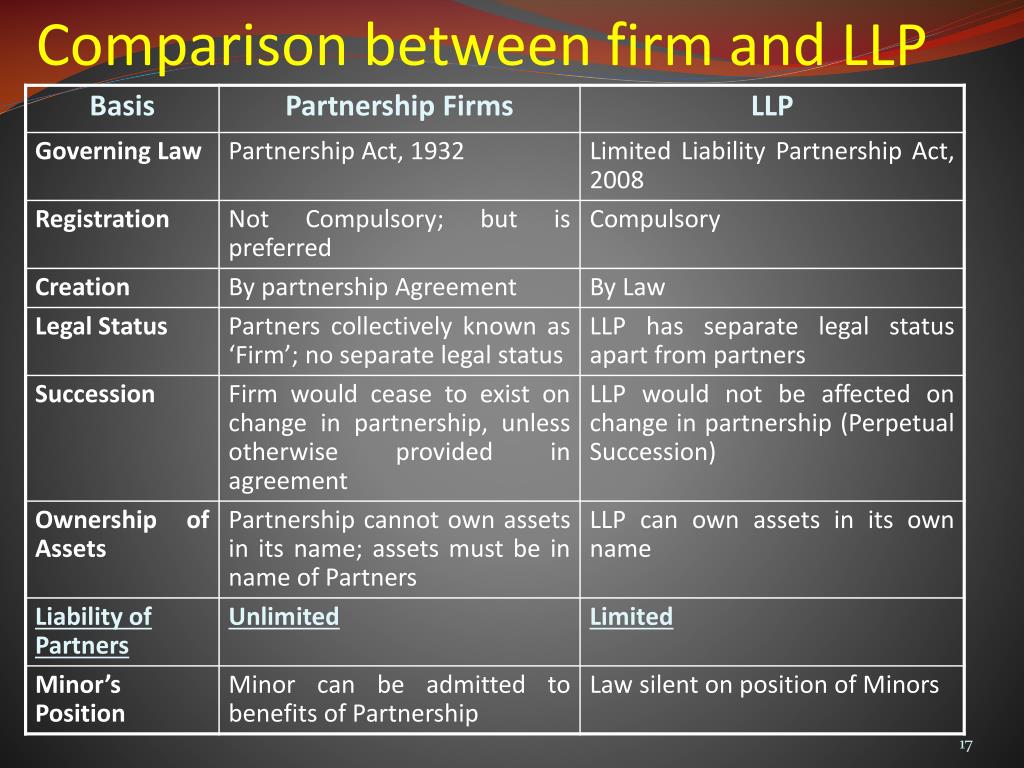

Comparison Of Llp With Company

Taxation Of Llps Including Its Restructuring By Milin Mehta Vadodara Direct Tax Refresher Course Pune Branch Of Wirc Of Icai 28 Th May Ppt Download

Incorporation Of Limited Liability Partnership Llp And Conversion I

2 Intricacies Of Alternate Minimum Tax Sec 115jc Minimum Alternate Tax Sec 115jb By Pawan Singla Ppt Download

Pin On Income Tax

Ppt Limited Liability Partnership Powerpoint Presentation Free Download Id 1658060

Are Foreign Investors Really Liable To Pay Mat The Hindu Businessline

Https Www Phplaw Co Uk S Terms Of Business July 2020 V2 Pdf

Discussion On Budget Updates Direct Taxes Ppt Download

Taxation Of Llp Under Income Tax Act 1961 Akt Associates

Source : pinterest.com